26 February 2026 | Macroeconomic and public finance outlooks for 2025–26 in the euro area: DPBs largely compliant with EU recommendations but risks of deviations

The Parliamentary Budget Office (UPB) published today a new Focus dedicated to the analysis of the 2026 Draft Budgetary Plans (DBPs) of the euro area countries, submitted last October. The Focus, together with an infographic, examines the macroeconomic and public finance forecasts for the 2025–26 period, comparing the projections of the DBPs with those of the Medium-Term Fiscal-Structural Plans (MTFSPs) and with the European Commission’s Autumn 2025 Forecasts. In addition, the analysis focuses on the developments in the four largest euro area economies (Italy, France, Germany and Spain, although the latter did not submit a DBP). UPB has also developed an interactive dashboard displaying the main macroeconomic and public finance indicators of the EU countries from 2016 to the present.

Economic growth: weak in 2025, moderate strengthening in 2026

According to the DBPs, 2025 was led by weak and uneven growth across euro area countries. After a stronger-than-expected first half of the year—also supported by front-loaded exports to the United States ahead of the introduction of tariffs—the global outlook weakened in a context of trade and geopolitical tensions.

For almost all countries, GDP is expected to expand in 2025, though at a moderate pace. France and Italy estimate growth of 0.7 and 0.5 per cent respectively, while Germany would stagnate and Austria would remain in recession. Spain, according to the European Commission, would instead record robust GDP growth (2.9 per cent), driven by domestic demand. In 2026, the DBPs foresee a moderate but widespread strengthening of economic activity, with a recovery in Germany and slight improvements for France and Italy.

Inflation: convergence towards 2 per cent

In 2025, growth in the GDP deflator would remain heterogeneous across countries, ranging from 4.3 per cent in Estonia to 1.5 per cent in France. Inflation would continue to ease in 2026: eleven out of eighteen countries would record GDP deflator increases of 2.5 per cent or less, compared with the ECB’s medium-term target (defined in terms of consumer price inflation) of 2.0 per cent.

Government deficits: above 3 per cent of GDP in 7 countries in 2025, in 8 in 2026 due to defence spending

In 2025, seven euro area countries indicate in their DBPs a deficit above 3 per cent of GDP; the Commission estimates an average deficit for the area of 3.2 per cent. Among the largest economies, Italy reports a deficit of 3 per cent of GDP, improving in comparison with 2024 and lower than the corresponding MTFSP target, thanks to a primary surplus of 0.9 per cent. France reports a deficit of 5.4 per cent of GDP, while Germany indicates 3.3 per cent. For Spain, in the absence of a DBP, the Commission estimates a deficit of 2.5 per cent of GDP.

In 2026, the number of countries with deficits above 3 per cent of GDP would rise to eight, mainly due to the planned increase in defence spending. The euro area’s aggregate deficit is expected to reach 3.3 per cent of GDP. Germany projects a deficit of 4.8 per cent of GDP; Italy 2.8 per cent, with a primary surplus of 1.2 per cent; and Spain 2.1 per cent. France revised its 2026 deficit upward to 5 per cent of GDP, from 4,7 per cent reported in the DBP, following the parliamentary approval of the budget law last February.

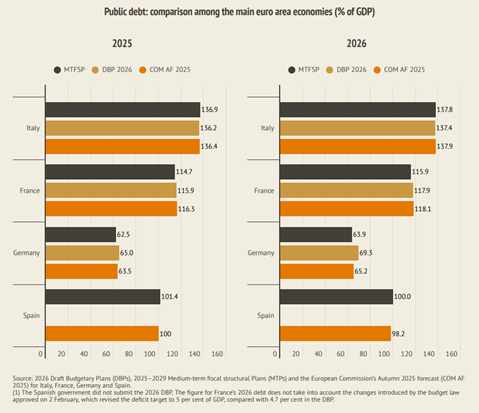

Public debt: euro area at 89.2 per cent of GDP, Italy and Spain below previous plans

According to the Commission, euro area public debt would reach 89.2 per cent of GDP in 2025, slightly higher than in 2024. Eleven countries remain above the 60 per cent threshold and six exceed 100 per cent of GDP.

Compared with previous trajectories, Italy and Spain present lower estimates for 2025–26. In Italy’s DBP, the debt-to-GDP ratio is indicated at 136.2 per cent in 2025 and projected at 137.4 per cent in 2026; for Spain, according to the European Commission, the ratio would decline to 98.2 per cent in 2026. France and Germany instead show higher values than those reported in their MTFSPs: German debt would rise to 69.3 per cent in 2026, also due to the activation of the national escape clause for defence; French debt would reach 117.9 per cent of GDP.

Net expenditure and the national escape clause for defence: Italy within the ceilings in 2025–26, others above in 2025 and 2026

The Commission assesses the overall fiscal stance of the euro area as broadly neutral in both 2025 and 2026, against the backdrop of differentiated national strategies. In 2025, most countries record net expenditure growth above the recommended ceilings; in 2026, the picture appears more heterogeneous. Italy estimates the net expenditure growth in line with the ceiling recommended by the EU Council in both years; Germany would exceed the ceiling in 2026, benefiting from defence-related flexibility; Spain exceeds the ceilings on an annual basis but remains within the deviation allowed by the new rules. The national escape clause for defence, activated for 17 Member States, allows the temporary deviation from the recommended maximum growth rate of net expenditure by up to 1.5 per cent of GDP over the period 2025–2028.

Overall compliance with EU recommendations but possible risks from the context

Overall, the Commission’s assessments indicate broad compliance of the DBPs with the EU Council Recommendations of July 2025. Nevertheless, risks of deviation remain for some countries, in a context defined by moderate growth, high debt levels and increasing spending needs for defence and strategic investments.