- The global economy expands despite uncertainty, but exports slow in 2026

- The Italian economy strengthens at the end of 2025, supported by domestic demand

- Italy’s 2025 growth would be lower than suggested by quarterly accounts, due to calendar effects

- The 2026 forecast improves, while the 2027 forecast is marginally revised downward

4 February 2026 | The Parliamentary Budget Office (UPB) today publishes the February Economic Outlook Report, which analyses—based on the most recent available indicators—the international and domestic business cycle, short-term trends, and the outlook for Italy. In particular, the macroeconomic forecasts for the 2025–27 period are updated in light of the latest cyclical developments, as processed by the PBO models.

International scenario: growth holds amid geopolitical uncertainty and a flight to safe-haven assets

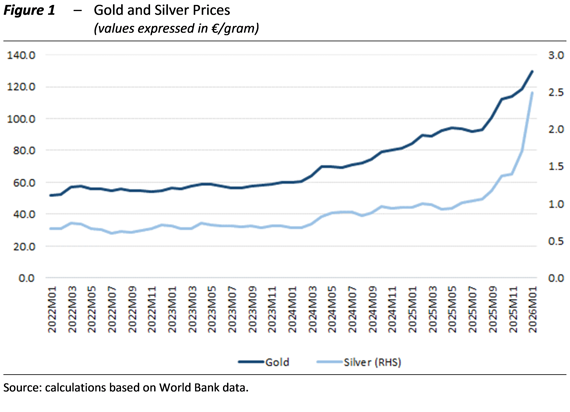

The international environment remains affected by high geopolitical uncertainty, with repercussions on energy prices, trade flows, and market expectations. In response, investors are increasing their exposure to safe-haven assets such as gold and silver, whose prices (Figure 1) have accelerated their upward trend underway for more than two years, even considering the decline observed in recent days.

Global economic activity remains uneven. In 2025, the United States recorded relatively solid growth of around 2 percent, while China—essentially meeting its 5 percent GDP target—maintained buoyant exports despite trade restrictions. In the euro area, production continues at moderate and differentiated rates across countries, with better results in economies supported by domestic demand compared with those more reliant on foreign trade.

The latest IMF estimates project global growth for 2026–27 to remain slightly above 3 percent, while in the euro area it would not exceed 1.5 percent. Despite expectations of stable global GDP dynamics this year, world trade is projected to slow sharply (from 4.1 percent in 2025 to 2.6 percent), penalizing more export-oriented economies.

Italy: 2025 growth at 0.5 percent based on annual data; upward revision to 2026 forecast

After near-stagnation in the middle quarters of 2025, Italy’s GDP accelerated to 0.3 percent in the fourth quarter, mainly driven by domestic demand. Based on preliminary quarterly national accounts, GDP increased by 0.7 percent in 2025; however, growth calculated on annual data should be lower by two-tenths of a percentage point. The difference reflects the adjustment for working days (not considered in annual accounts), as there were three fewer working days in 2025 than in 2024.

Accordingly, the UPB’s preliminary estimate places 2025 GDP growth at 0.5 percent based on annual data.

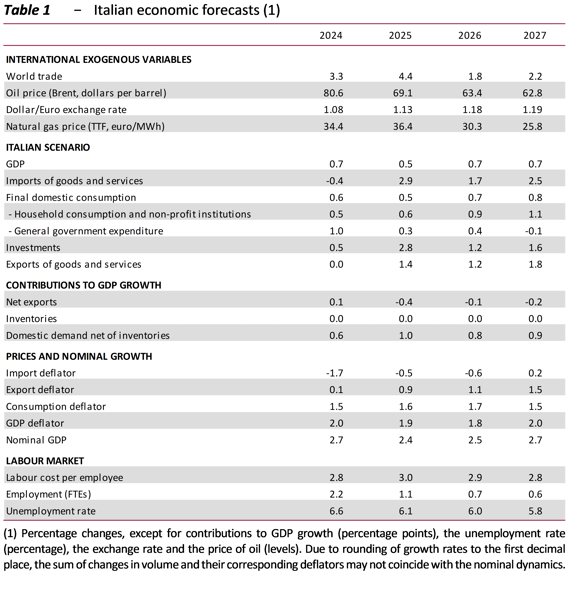

UPB macroeconomic forecasts then point to strengthening growth of 0.7 percent in 2026, supported by domestic demand and in particular by the implementation of the NRRP (National Recovery and Resilience Plan), with a similar rate projected for 2027 (Table 1). Compared with the autumn estimates made by the UPB for the endorsement of the Ministry of Economy and Finance (MEF) forecasts in the DPFP, the outlook has improved for 2026, reflecting international assumptions that are less penalizing for external demand and lower consumer prices. On the basis of the same updated assumptions, the 2027 GDP forecast has been slightly revised downward.

Exposure to downside risks remains high, mainly related to the global environment as well as financial market sentiment and climate change.

Labour market: positive trend continues, but real wages still below pre-pandemic levels

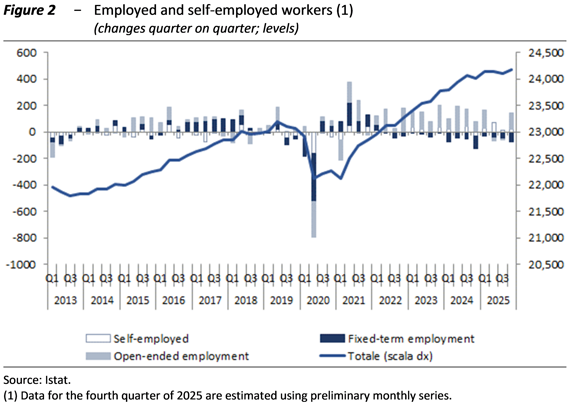

In the summer, labour input increased (Figure 2), driven by a recovery in hours worked per employee, particularly in manufacturing and services. In the forecast scenario, employment would continue to expand at a moderate pace, with the unemployment rate stabilizing at around 6 percent. Wage growth remains moderate, leaving a wide negative gap in real wages compared with the pre-pandemic period.

Inflation in Italy remains contained (1.5 percent in 2025) and below the euro-area average. Household consumption grows gradually, although the cautious attitude of households is confirmed by the saving rate (11.4 percent in the third quarter of 2025, about four percentage points higher than pre-pandemic levels), while expectations of households and firms remain oriented toward stability. The investment rate remains around 23 percent of GDP, a relatively high level by historical standards.

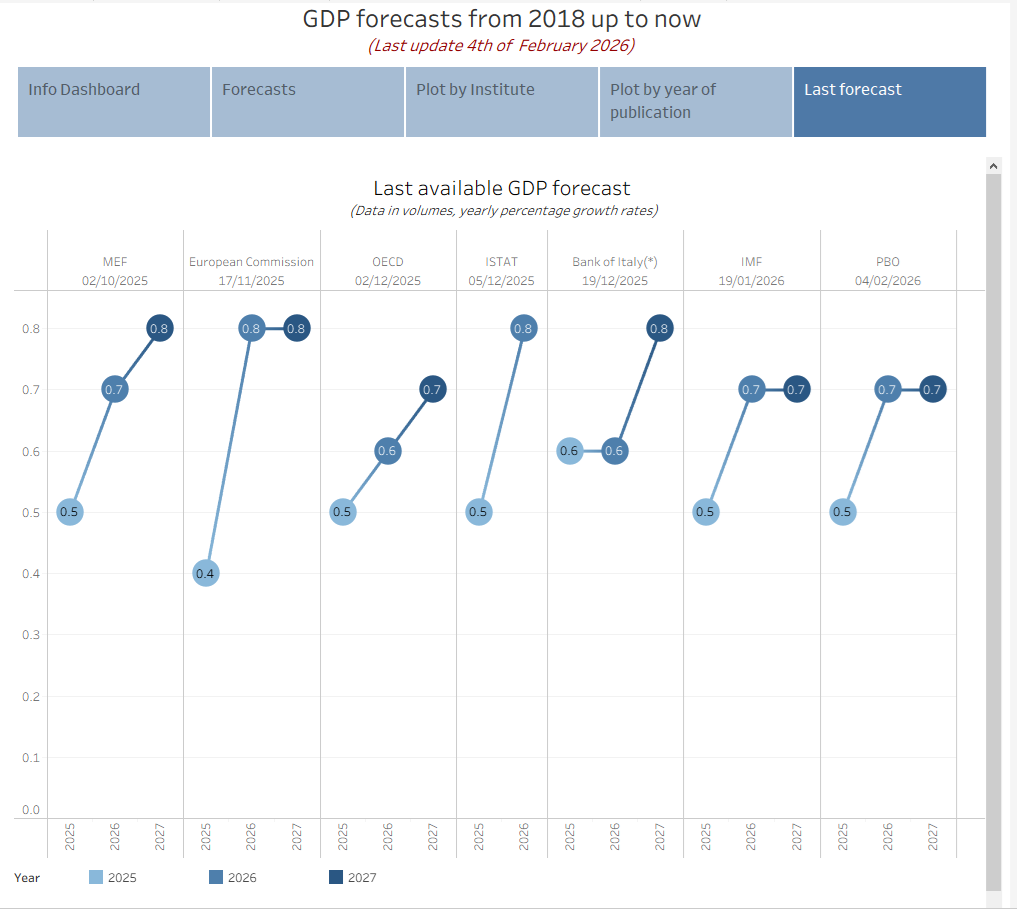

The infographic on growth estimates by major institutional forecasters is updated accordingly.