26 March 2025 | The Parliamentary Budget Office (PBO) held a hearing today before the Senate Finance and Treasury Committee as part of the fact-finding inquiry into the management of the fiscal inventory by the collection agency and the review of Bill No. 1375 (Provisions concerning the long-term installment payment of tax, social security, and other liabilities assigned to the collection agent). The document presented today by PBO Councillor Valeria De Bonis provides, after a brief overview of the measures affecting outstanding liabilities since 2016 (facilitated settlements and cancellations) and those proposed in the bill under review, a reconstruction of the evolution over recent years of collected, written-off, and residual receivables. It also offers considerations regarding the factors influencing the accumulation of receivables within the fiscal inventory, Italy’s international positioning in this regard, and how the measures proposed in the bill align with the reform process initiated with the legislative decree implementing the enabling law for tax reform.

The bill introduces a facilitative measure for the settlement of outstanding liabilities akin to those previously enacted, albeit more generous—particularly due to the extended time frame granted for payment. Its intended objectives are to reduce the volume of receivables entrusted to the collection agent and to support households and businesses facing financial hardship with unpaid taxes that had been duly declared, which tend to grow over time due to the accumulation of penalties and interest. However, no mechanism is envisaged to effectively target the measure exclusively to such distressed taxpayers. The measure fits within a broader context of tax collection that has become increasingly complex over time, owing to the layering of legislative amendments, and the ongoing reform process initiated by Legislative Decree No. 110/2024, implementing the enabling law for tax reform.

The numerous legislative interventions introduced over time do not appear to have significantly addressed the inefficiencies inherent in enforced collection, with evident repercussions on the size and quality of the stock of receivables entrusted to collection, and on the revenues of the general government. On one hand, these interventions have generally favored taxpayers in a non-selective manner — including those capable of meeting their obligations — while allowing the disposal of only a modest portion of the receivables assigned over time to the collection agent. On the other hand, they have complicated the tasks of the collection agent due to the accumulation of provisions (e.g., differing collection procedures, re-admittance of taxpayers previously excluded from relief, cancellation of liabilities included in ongoing settlement or installment plans, and progressively longer installment plans), without enhancing enforcement efficiency. Instead, such measures have made the collection function increasingly resemble a liquidity support mechanism for taxpayers. The repeated and layered implementation of increasingly generous relief measures and write-offs contributes to fostering expectations among taxpayers that unpaid taxes will eventually be forgiven or resolved under even more favorable conditions. This undermines both ordinary and enforced collection efforts and negatively affects overall revenue and tax compliance.

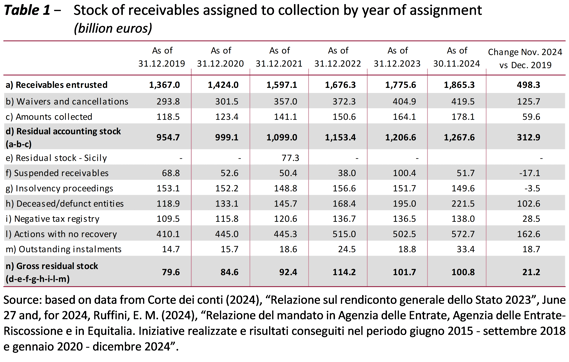

As of the end of November 2024, the total receivables assigned to the collection agent amounted to over €1,865 billion (+36.5 percent compared to the end of 2019), while actual collections stood at approximately €178 billion (9.5 percent), indicating limited effectiveness of enforced collection actions (see Table 1). These liabilities largely consist of individual debts below €1,000, primarily involving individuals. The total volume is influenced by several factors: the large number of individual receivables entrusted annually to the collection agent; often lengthy timelines for processing each item; the complex procedure for certifying uncollectibility; a progressively narrower scope for recovery actions; and inefficiencies in both voluntary and enforced collection mechanisms.

As of the same date, the residual accounting stock—net of amounts collected, cancelled, or written off—amounts to €1,267.6 billion (68 percent of the total assigned), up 32.8 percent from 2019. Of this, the Revenue Agency-Collection (AdER) estimates that only €100.8 billion (5.4 percent of total assignments, 8 percent of the residual accounting stock) is the gross residual stock deemed to have a higher degree of collectibility. This includes approximately 291 million individual receivables contained in around 175 million bills, debit notices, or enforcement assessments.

The measures enacted in recent years — some of which are reiterated in the current bill — have not significantly contributed to the disposal of receivables. Revenues from facilitated settlements, except for the more advantageous “Rottamazione Quater”, have fallen short of expectations due to the high share of taxpayers failing to complete full payments after joining the program. Overall, the measures have reduced the stock of receivables by about €112 billion as of March 2024—of which €30 billion through concluded relief schemes (rising to €31.6 billion by November 2024) and over €82 billion through write-offs. The annual accumulation of new receivables remains substantial.

The repeated implementation of facilitated settlement or debt write-off measures can generate expectations of future amnesties, negatively impacting voluntary payments, standard collection, and enforcement activities, and ultimately tax compliance. Moreover, the implications of these measures on the overall equity of the tax system should not be overlooked. Such interventions should be accompanied by improved efficiency in both enforcement mechanisms and incentives for voluntary tax compliance.

A substantial reduction of the receivables stock requires a comprehensive reform. This should include, among other elements, a revision of the procedures for certifying the uncollectibility of receivables and the introduction of an automatic cancellation system for definitively uncollectible debts. Such reforms would allow the collection agent to focus efforts on receivables with a higher probability of recovery. Furthermore, the Revenue Agency should be enabled to fully exploit its data capabilities by ensuring the interoperability of databases. This would allow for a more timely and accurate understanding of receivables and their related taxpayers, and more effective risk identification and analysis of tax evasion and default. Legislative Decree No. 110/2024, implementing the enabling law for tax reform, moves in this direction. It provides, among other things, for annual planning of collection procedures, an automatic write-off mechanism for liabilities assigned to AdER at the end of the fifth year following assignment, and the possibility for the collection agent to request early discharge in cases of bankruptcy, liquidation, or verified insolvency of the debtor. It also establishes a Commission for the analysis of the inventory of outstanding liabilities, tasked with identifying solutions for their partial or total discharge within a specified timeframe.

Any evaluation of the current bill must take into account its alignment with the broader reform framework. There appears to be a potential conflict between the introduction of a new relief measure and the anticipated discharge of all or part of the inventory by 2031, based on the Commission’s proposals. Additionally, the option granted to local authorities to introduce their own relief measures may be more appropriately addressed within the context of delegated fiscal reform concerning local taxation.