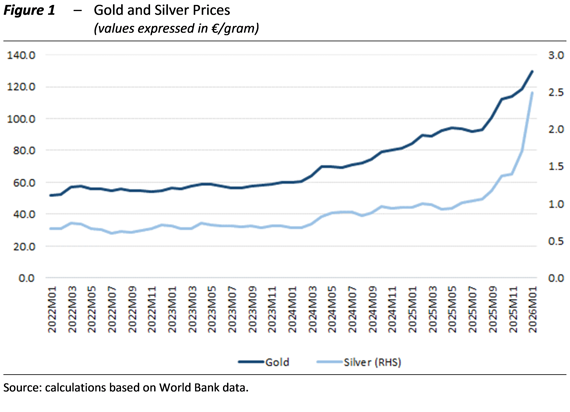

4 February 2026 | The international environment still appears dominated by high geopolitical uncertainty, which mainly affects energy prices, trade flows, and financial market expectations. In this context, investors are showing growing interest in safe-haven assets, whose prices (Figure 1) have accelerated in recent months and displayed greater volatility in recent days. Global growth remains fragmented. In 2025, economic activity in the United States remained relatively solid, while in China exports continued to be very dynamic despite protectionism. In the euro area, production continues at generally moderate rates, differing across countries, with stronger performance in those driven by domestic demand. In its latest forecasts, the International Monetary Fund (IMF) expects global growth to continue at a rate slightly above 3 per cent, while in the euro area it would not exceed 1.5 per cent. Despite expectations of stable global GDP growth this year, a sharp slowdown in world trade is projected (from 4.1 per cent in 2025 to 2.6 per cent).

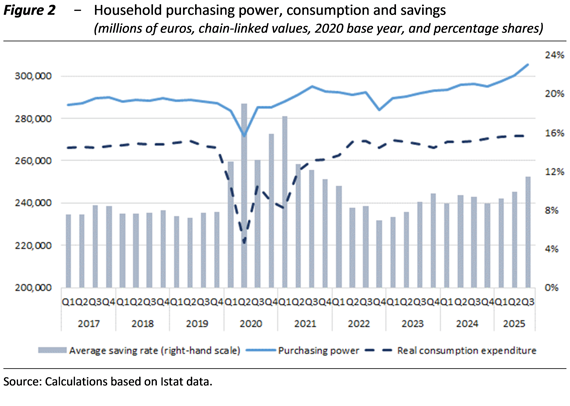

In Italy, economic activity was moderate in the middle quarters of 2025, when the saving rate increased again, reflecting caution in household spending decisions (Figure 2). The cyclical phase strengthened in the final part of the year, when domestic demand picked up and GDP accelerated to 0.3 per cent. Overall, in 2025 GDP increased by 0.7 per cent based on quarterly data adjusted for working days, while according to annual data (to be released by Istat on 2 March) the change should be lower by a couple of tenths of a per centage point due to calendar effects.

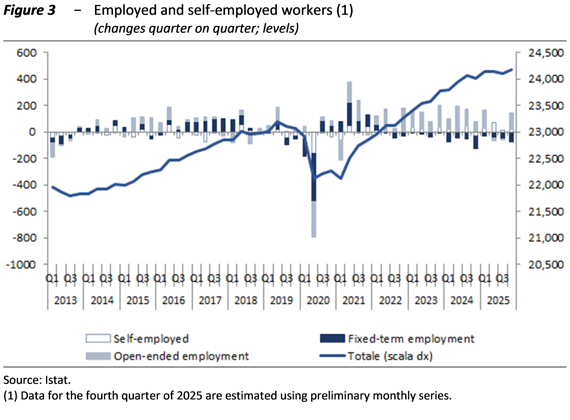

During the summer, labour input increased (Figure 3), supported by a recovery in hours worked per employee, particularly in manufacturing and services. Wage growth remains moderate; therefore, the negative gap in real wages compared with the pre-pandemic period remains wide. Italian inflation continues to be modest and lower than the European average; household and business expectations remain oriented toward stability.

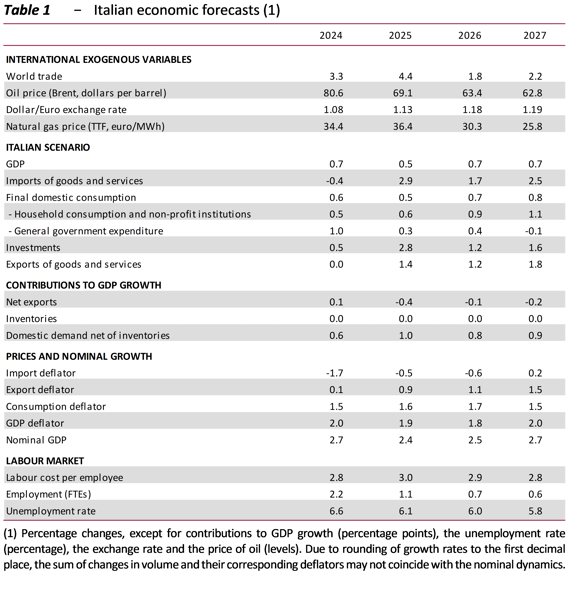

The update of the Parliamentary Budget Office (PBO) macroeconomic forecasts for Italy indicates that GDP would strengthen gradually, accelerating from 0.5 per cent in 2025 to 0.7 per cent in 2026–27 (Table 1). Compared with the autumn projections, prepared during the endorsement exercise of the Ministry of Economy and Finance (MEF) forecasts, the estimates have been revised upward for 2026 and slightly trimmed for 2027. The update of international assumptions points this year to less unfavourable external demand dynamics and lower consumer prices. The Italian macroeconomic outlook remains exposed to downside risks, largely attributable to the global environment, as well as to financial market conditions and climate change.